The fee and payment system in medicine is a big black box. Patients don’t know the true costs of medical care and we have no clue what bill the patient gets when we order all those tests. There’s a black box with financial advisors also: fees. I have not yet met a physician who knows exactly what fees he’s paying to his financial advisor.

The fee and payment system in medicine is a big black box. Patients don’t know the true costs of medical care and we have no clue what bill the patient gets when we order all those tests. There’s a black box with financial advisors also: fees. I have not yet met a physician who knows exactly what fees he’s paying to his financial advisor.

So let’s open the financial advisor black box and look at the actual fees you’re paying. Let’s assume you have $500,000 to invest.

Commission-Based Advisors

A typical class A share mutual fund’s commission is about 5%. The advisor spreads your money across several funds, so on $500,000 you’ve just paid a $25,000 commission up front. That means you’ve only invested $475,000 of your money. Every time you invest new money, you get hit with another commission. Then, if the advisor switches you out of your current funds into new commission based funds, you get hit with the commission on the entire portfolio, not just the new money. For example, after several years of contributions your portfolio is now $750,000. If the advisor switches you to new funds you’ll pay the commission on the entire $750,000 – as high as nearly $40,000! You don’t see this because you don’t get an invoice like you do with your electric bill. Some physicians naively assume that they aren’t “paying anything” to these advisors. Wrong!

The upfront commission doesn’t include the annual mutual fund expenses. Most commission-based advisors use high expense mutual funds – 1.5% annual fund expenses are common. This fee isn’t a direct fee; rather, high mutual fund expenses result in lower portfolio returns. So in the first year you’ll pay $7,500 in mutual fund fees. That’s on top of the 5% commission for a whopping $32,500 in the first year. Subsequently you’ll continue to pay the mutual fund expenses and included in that is the trailing commission, or 12b-1 fee, of 0.25% to 1% annually. That’s between $1,250 and $5,000 annually in trailing commissions on your $500,000 portfolio.

Fee-Only Advisors

Fee-only investment advisors, who are supposed to act as fiduciaries to you, typically charge an assets under management fee based on the value of your portfolio. Here is a typical fee structure:

1% on assets up to $1 million

0.8% on assets between $1 million and $3 million

0.7% on assets between $3 million and $5 million

0.5% on assets above $5 million

You might mistakenly think that the fee goes down as your portfolio goes up. That is not true. While the blended percentage goes down, the actual dollar amount you pay goes up. For example on a $500,000 portfolio you will pay $5,000. At $1 million the fee is $10,000. At $2 million the total advisor fee is $18,000 ($10,000 on the first $1 million and then $8,000 on the next million).

Even with fee only advisors you have to add the mutual fund expenses on top of this. Most fee only advisors also use high cost funds but because there is no 12b-1 fee, the fund expenses are lower than with commission based advisors. Mutual fund expenses of 1% are typical.

So the total fees for a $500,000 portfolio are $10,000 ($5,000 advisor fee + $5,000 mutual fund expenses) or 2% of your portfolio. At $1 million, it’s $20,000. At $2 million it’s $38,000. As you can see this gets really expensive.

Many advisors try to make you think that there’s some sort of mystery to managing a $2 million portfolio versus a $500,000 portfolio so they can justify their high fees. There is some more complexity but not anywhere near what these advisors claim. And if a fee only advisor is supposed to act as a fiduciary, doesn’t part of that duty to you involve charging reasonable fees? Fee only advisors are supposed to act in your best interests but many bury their heads in the sand when talking about their own fees. From your perspective, high fees eat into your portfolio returns and ultimately your retirement.

Of course you can’t just look at the fee. You also have to look at the value that you get for the fee you’re paying. If you have a competent and ethical advisor, the value comes from the objective advice and discipline you get by having the advisor. From the advisor’s perspective the fee has to go up because some of the advisor’s expenses are tied in to the amount of assets he manages. As the advisor manages more assets certain fees like custodial fees and insurance costs go up so the advisor has to charge more for higher portfolio values.

So what is a reasonable fee? I believe that the advisor fee plus the mutual fund expense should total less than one percent.

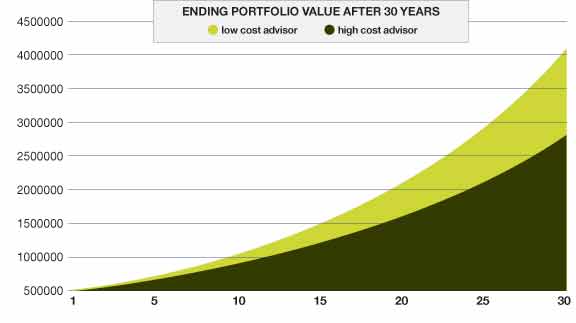

Just take a look at the following graph to see what your ending portfolio is for two different advisors. The typical fee only advisor charges the fee schedule listed above and the average mutual expense is 1% annually. The second advisor charges 0.5% and uses low cost mutual funds with annual expenses of just 0.2%. Assume you start with a $500,000 portfolio. Before fees each advisor’s portfolio returns 8% annually. The lower cost portfolio results in over $1.2 million in higher portfolio value after 30 years.

Let’s put this into a more practical perspective for EPs. Suppose you make $1500 per shift and $50 for an emergent intubation. You would have to work over 800 more shifts and do more than 24,000 more intubations with the higher cost advisor. Now do you think advisor fees matter?

Setu Mazumdar, MD practices EM and he is the president of Lotus Wealth Solutions in Atlanta, GA www.lotuswealthsolutions.com

7 Comments

I hope Dr. Mazumdar is paying EP Monthly for this “advertorial.” If not, I’d like to see my own financial advisor given the opportunity to be featured like this.

I cannot believe this article was ever published given the extreme inaccuracies given here. Dr. Mazumdar has a right to his opinion but at least give factual information to start.

First, Dr. Mazumdar overlooks the breakpoint feature when it comes to A share investments. Yes, some A shares may charge as much as a 5% fee in investments but that goes down with larger investments. For example: American Funds has equity mutual funds with a max sales charge of 5.75% but on $500,000 the fee would only be 2% or $10,000 NOT $25,000.

Second, clients are free to move their funds to various mutual funds within the same family at NO COST. This means that if market conditions or personal situations change the client may change their allocation without paying the sales charges again. If an advisor changes mutual fund companies completely this is a practice call switching that will get that advisor into hot water with their compliance department and/or FINRA.

I have no idea where Dr. Mazumdar gets a figure of the average mutual fund expense being 1.50% either. Take American Funds for example again, The Growth Fund of America costs investors .68% per year – LESS THAN HALF. Also, he outright lies saying that 12b-1 fees are .25%-1%. Class A mutual funds are .25% maximum! Some are less than that even. Only B and C shares provide 12b-1 fees of up to 1% and he doesn’t even address those here.

Finally, he suggests using mutual funds with annual expenses of .2% – these are called index funds or NON MANAGED FUNDS. To compare the performance of a portfolio of managed funds versus non managed funds of 30 years and assume all things are equal except the fee is plain stupid. The whole reason why advisors recommend funds that are managed funds is to have active managers work to achieve higher returns and beat their benchmark index!

What a terrible piece of work and even worse periodical to publish this crap.

Mr. Wright,

Looks like I hit a nerve! That’s great because physicians deserve to be told the truth about the way financial advisors operate and the poor advice many physicians receive from advisors.

I’m assuming that you are a financial advisor based upon the comments you’ve written. In that case I seriously question your competency. Let’s take your diatribe and rip it apart piece by piece.

You state that I am “stupid.” I admit I’m not the smartest guy in the world, but l did get accepted to Johns Hopkins medical school–among the top medical schools in the world–at the age of 19 and graduated from there. So I probably have a reasonable level of intelligence. I also specialized in emergency medicine and practiced for a number of years. The vast amounts of data that an emergency medicine physician expertly and accurately analyzes in record time during a single emergency department shift far exceeds what your brain as a financial advisor can handle in a whole month. Think I’m kidding? Join me on a Friday night shift in the ER–you’ll probably have multiple episodes of urinary and bowel incontinence since you won’t be able to handle the stress (I suggest you bring a few extra pairs of underwear and lots of deodorant). I also passed the CFP® Certification Examination, something which your industry regards highly.

You sound like a politician not only with the language you use with words such as “crap” but also because you come up empty handed when presenting any academic evidence to back up your claims.

First, you state that the “whole reason why advisors recommend funds that are managed funds is to have active managers work to achieve higher returns and beat their benchmark index.” This suggests that you believe in active investment strategies, which attempt to beat the market index by either stock picking or market timing, or by picking the winning mutual fund managers ahead of time. If you believe in active management, you need to do 3 things:

Wear a shirt that says on the front “I CAN’T ADD.”

Wear a shirt that says on the back “I CAN’T READ.”

Wear a cap that says “I CAN’T THINK.”

The academic literature is clear on this issue–the majority of actively managed funds underperform their respective market over a 5 year period. Standard and Poors keeps track of active funds and calculates what percent beat the index. In their latest study they conclude that “the only consistent data point we have observed over a five-year horizon is that a majority of active equity and bond managers in most categories lag comparable benchmark indices.” A great paper 20 years ago by Williams Sharpe–a Nobel Prize winner–showed that by simple addition and subtraction it is mathematically impossible for the average active investor to beat a passive investor. A study 3 years ago by Fama and French from University of Chicago and Dartmouth showed that the percent of active fund mangers that beat the market was no higher than what is expected by random luck. There are lots more academic studies drawing similar conclusions.

Second, Morningstar and other sources stated that the average mutual fund expense ratio a few years ago was about 1.5%. Vanguard estimates it as 1.2% to 1.3%. Since it appears that you don’t know basic math, an average usually means that there will be some funds with an expense ratio below the average and other funds with expense ratios above the average. I did not state that all funds have expenses of 1.5%. Regarding 12b-1 fees I stated that they are between 0.25% to 1% annually and that is a true statement. In other articles I have addressed Class B and C shares–again perhaps you should read and think before you write. You also state that the breakpoint might “only be 2% or $10,000” if you buy $500,000 of a class A share fund. That’s far too high a fee for a client to buy a fund. I wish emergency medicine physicians could make that kind of money by saving someone’s life! And then you ignore the annual expense ratio on top of that sales charge. You also fail to discuss all the indirect fees you pay by using active funds–poor tax efficiency, underperformance, lack of diversification, etc.

Continued below…

That gets me to a much more important point which you and many commission based advisors usually fail to bring up with clients–the inherent conflict of interest that is created when an advisor is paid by the funds he sells. Perhaps you are afraid of the “F” word: fiduciary. You see, physicians are fiduciaries to patients–we are legally and ethically required to place a patient’s interest above our own. If you get paid by selling financial products you have an inherent conflict of interest and are not acting as a fiduciary to the client and are not placing the client’s interest first. How objective are your recommendations if your compensation is tied to financial products? That’s analogous to a physician getting paid by the drugs he recommends to a patient instead of the advice he gives. But you didn’t mention that at all did you?

Physicians deserve better advice from financial advisors. My passion for writing this column stems partly from exposing what goes on in the financial services industry so I can educate other physicians and make them better investors.

So you can dislike this publication, but I think the authors and editors of this publication do a fantastic job of educating physicians. Maybe you should go to medical school so you can understand the other articles–that is if you can get in.

Finally, here’s a piece of advice from Mark Twain you may want to heed:

“It is better to keep your mouth closed and let people think you are a fool than to open it and remove all doubt.”

Dr. Mazumdar’s post is right on the money. I’m a financial advisor, author, and most important to this discussion, a professor of financial planning. My graduate level financial planning education comes from Kansas State’s top ranked program and the University of Chicago. I can validate with confidence that Dr. Mazumdar’s claims are right on the money. I am familiar with the research he sites and also with the commonly erroneous claims made by Mr. Wright. I have no relationship with Dr. Mazumdar but if I had to choose between he and Mr. Wright, the doctor would win my business. Thanks for your post! Keep educating your peers!

There are many financial advisors available in the market but it is in your hands to choose the best one because it effects your financial business.

Many people believe that investing in mutual funds is a good plan to save money for their retirement time. It is worth mentioning that there are some things to taken into account earlier to investing your money.